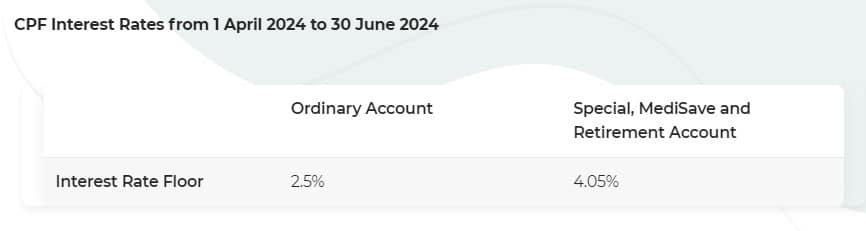

CPF Q2 rates: Special, MediSave & Retirement Accounts dip to 4.05%

CPF announces 4.05% interest for Special, MediSave, and Retirement accounts from 1 April to 30 June, a slight dip from the previous quarter's 4.08%.

The Central Provident Fund (CPF) has set the interest rate for Special, MediSave, and Retirement accounts at 4.05% per annum for the period between 1 April to 30 June.

This marks a slight decrease from the previous quarter's rate of 4.08% (1 January to 31 March).

In a joint statement on Tuesday (12 March), the CPF Board and Housing Board explained that the interest rate for these accounts, linked to the 12-month average of 10-year Singapore Government Securities plus 1%, surpasses the floor rate of 4%.

For the second quarter of 2024, the interest rate for Ordinary Account (OA) savings remains unchanged at 2.5%.

"The Government will continue to ensure that the CPF interest rate pegs remain relevant in the prevailing operating environment while taking into consideration the longer-term outlook,” the statement said.

The concessionary interest rate for HDB housing loans, tied to 0.1% above the OA interest rate, will remain steady at 2.6% per year from 1 April to 30 June.

CPF members below 55 years old will continue to earn an additional 1% interest on the initial S$60,000 of their combined account balances, capped at S$20,000 for the OA.

Members aged 55 and above will maintain an additional 2% interest on the first S$30,000 of their combined balances, capped at S$20,000 for the OA, and an additional 1% on the subsequent S$30,000.

In Parliament on 2 August 2022, Manpower Minister Dr Tan See Leng affirmed that if pegged rates surpass floor rates, members will accordingly earn higher interest rates on their CPF savings.

He said the government has upheld a floor rate of 4% for the three accounts since 2008.

WP MP Louis Chua renewed call for reform in Ordinary Account interest calculation

On 4 March, participating in the Committee of Supply 2024 debate for the Manpower Ministry (MOM), Workers’Party Member of Parliament for Sengkang GRC Mr Chua Kheng Wee highlighted a significant disparity in the returns of the CPF for its members when compared to the Government of Singapore Investment Corporation (GIC), which boasts a 20-year annualized nominal rate of return of 6.9%.

Mr Chua questioned the feasibility of allowing Singaporeans to co-invest a portion of their savings, contemplating the existing CPF Investment Scheme (CPF IS).

However, Dr Tan dismissed the proposal and cautioned that even though GIC has outperformed CPF interest rates over the past 20 years, there’s no assurance that this trend will persist in every future year.

He emphasized that passing these returns directly to CPF members could result in significant year-to-year fluctuations in the interest rates received by members.

Mr Chua reiterated the call for the reform of the outdated and archaic formula used to compute the interest for the Ordinary Account.

“This was last changed in 1999 when the ratio of fixed deposits to savings was updated from 50/50 to 80/20 to reflect the longer duration that CPF OA monies remained with the CPF Board. A reform is long due,” Mr Chua stated.

The concern is raised over the CPF deeming the deposit interest rates to be an unbelievable 0.66% despite higher market rates.

He also proposed the Implementation of the Lifetime Retirement Investment Scheme (LRIS) to enhance CPF returns, a suggestion put forward by a CPF review panel back in 2016 as an alternative to the CPF Investment Scheme.

In response, Dr Tan reassured that the government continues to introduce measures to enhance retirement savings for older, lower-wage earners, homemakers, and caregivers.

He highlighted positive developments in CPF members’ savings, noting that over 70% of active members have set aside the Full Retirement Sum (FRS) by the age of 55.

Addressing concerns about the closure of the Special Account (SA) for workers aged 55 and above next year, Dr Tan explained the context and impact of this decision.

He clarified that only a small percentage of affected members would face challenges in fully transferring their savings to their Retirement Accounts (RA). Both the Special Account and Retirement Account currently earn 4.08% interest per annum.

“It is a matter of principle … it is not about savings costs for the government,” said Dr Tan.

Regarding Mr Chua’s call for the implementation of the proposed LRIS, Dr Tan acknowledged potential risks for retirees if implemented.

Dr Tan also responded to suggestions to reevaluate how the Ordinary Account interest rate is determined.

“The government is aware that the OA interest rate has remained relatively stable, while the use of market instruments of comparable risk and duration has increased.”

He urged a long-term perspective, emphasizing that the CPF has consistently paid 2.5% interest, with the annual Ordinary Account interest rate being 1.7 percentage points higher than 12-month fixed deposit rates from 1999 to 2021.

“Nevertheless, we are monitoring the situation, and will continue to review CPF interest rates periodically, to ensure their relevance in the prevailing operating environment.”

Dr Tan emphasized the limitations of relying solely on historical returns when evaluating investment performance.

Despite GIC outperforming CPF interest rates over the past 20 years,he cautioned that there is no assurance that GIC’s future returns will consistently surpass CPF interest rates annually.

“So if we pass some of these returns directly to members, you would then appreciate the fact that there would be significant year-to-year fluctuations in the interest rate that members receive.”

He explained that the government has used its buffer of net assets to ensure that CPF members receive fair and stable interest rates to grow their CPF balances for retirement adequacy.

He defended the cautious approach, stating that it is not a fault but a necessity.

“I don’t think it’s a fault is that we are very very cautious because these are our members hard earned monies,” he said.