Netizens voice unhappiness over CPF policy's "shifting goalposts"

Online community voices disappointment over DPM Lawrence Wong's CPF changes, criticizing "shifting goalposts" that hinder early savings access and higher interest rates for members.

A segment of the online community has expressed disappointment following Deputy Prime Minister Lawrence Wong's recent announcement regarding significant changes to the Central Provident Fund (CPF).

Critics are dissatisfied with what they perceive as another instance of "shifting goalposts," arguing that it makes it more challenging for CPF members to access their savings earlier and earn a higher interest rate.

Some netizens have highlighted that the removal of the CPF Special Account (SA) for individuals aged 55 and above eliminates a loophole that allowed certain CPF members to allocate more funds to the higher interest-earning Special Account and Retirement Account.

These accounts yield an annual interest of 4.08 per cent, a notable increase compared to the 2.5 per cent annual interest earned in the Ordinary Account.

To recap on the CPF system, When a CPF member turns 55 years old, a Retirement Account (RA) will be created.

Currently, savings from the member's Special and Ordinary Accounts, up to the Full Retirement Sum (FRS), are transferred to the RA to create a retirement sum, ensuring a monthly income in their old age.

The remaining savings in the Special and Ordinary Accounts can be withdrawn any time after the member turns 55 years old, subject to the applicable withdrawal rules.

SA is to accumulate savings for a member's retirement.

The CPF member may also apply to withdraw their RA savings (excluding top-up monies, any government grants received and interest earned) above the Basic Retirement Sum (BRS) if he/she owns a property with a remaining lease that can last till age 95.

In his budget announcement last Friday, DPM Wong outlined several changes to the CPF, poised to reshape the retirement savings landscape for Singaporeans.

Among these changes, a pivotal modification stands out: the discontinuation of the Special Account (SA) for individuals aged 55 and above, set to take effect next year.

This adjustment aims to streamline retirement savings into fewer accounts, specifically the RA, and to address the redundancy of the SA for those who have reached the age of eligibility for RA creation.

Under the new scheme, funds in the SA will be transferred to the RA to meet the full retirement sum, with any surplus funds redirected to the Ordinary Account (OA), which yields a lower interest rate.

"Moving the goalposts"

The recent significant changes have sparked a heated discussion on online forums.

An observation on the Singapore HardwareZone forum makes it evident that there are sentiments indicating that the government is once again "moving the goalposts," attempting to close a perceived "loophole" for certain members who were benefiting from higher interest rates in the SA.

Netizens have pointed out that this move also prevents members from utilizing a "shielding" tactic that allows them to allocate more funds to the higher interest-earning SA and RA.

While DPM Wong had previously explained that the closure of the SA is aimed at "rationalizing the CPF system," some netizens hold the view that the government may be attempting to reduce interest payments on the SA.

MOF clarifies interest rate principles for SA withdrawals

The Ministry of Finance (MOF) in a statement explained that savings in the SA, some of which can be withdrawn anytime for members aged 55 and older, should not be earning a higher interest rate.

According to the ministry, “As a principle, only savings that cannot be withdrawn on demand should earn the long-term interest rate, and savings that can be withdrawn on demand should earn the short-term interest rate.”

While SA savings up to the Full Retirement Sum will be transferred to the Retirement Account (RA), MOF emphasized that these savings will continue to earn the long-term interest rate.

Any remaining SA savings will be moved to the Ordinary Account (OA), where they remain withdrawable and earn the short-term interest rate.

Members have the option to transfer their OA savings to their RA at any time, up to the Enhanced Retirement Sum.

MOF defended that once in the RA, the funds are dedicated to higher retirement payouts and earn a higher interest rate.

This implies that after age 55, the RA becomes the primary CPF account for a member's retirement, while the OA remains available for withdrawal at any time.

According to information shared by the CPF Board, for members continuing to work after age 55, CPF contributions will be directed to the RA instead of the SA, allowing members to set aside their Full Retirement Sum (FRS).

Once the FRS is met, these CPF contributions will be allocated to the OA and become eligible for withdrawal.

Anticipation of additional adjustments raises concerns

There is speculation within certain discussions that the goalposts will inevitably shift concerning retirement saving. It is suggested that further changes might occur within the next three to five years.

Netizen expressed disappointment with option to keep SA eliminated

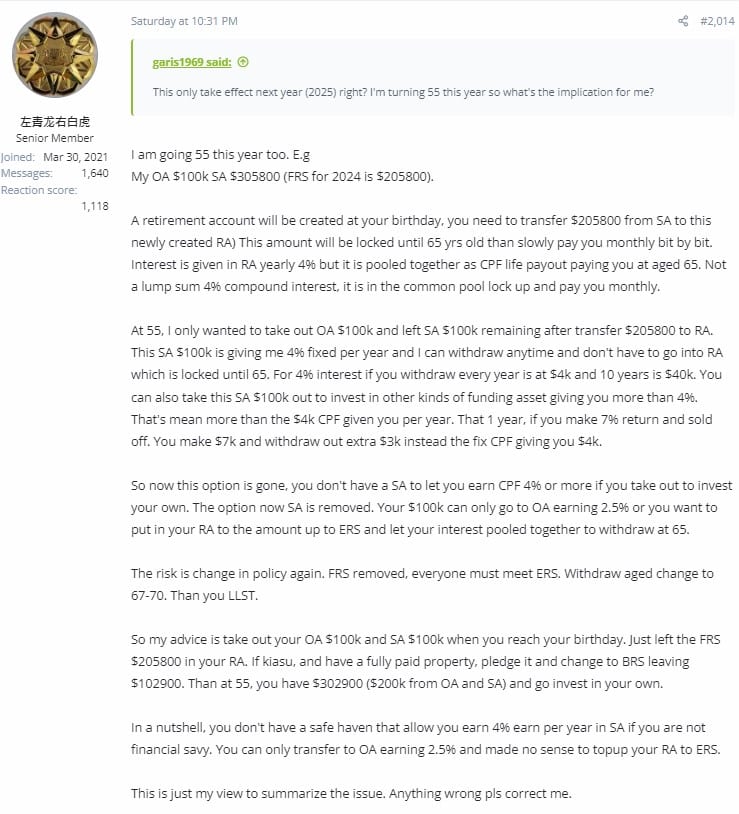

Notably, one netizen, expressed concern and dissatisfaction with the closing of SA, provided a detailed analysis of the impact on their financial strategy, particularly in terms of retirement planning.

The netizen claimed that he initially wanted to withdraw only the OA funds at 55, leaving $100k in the SA after transferring $205,800 to the RA.

This would allow him to benefit from the 4% fixed interest rate in the SA and have the flexibility to withdraw at any time.

He expressed disappointment that the option to keep funds in the SA to earn a fixed 4% interest or use it for personal investments is now eliminated.

Speculation on policy change

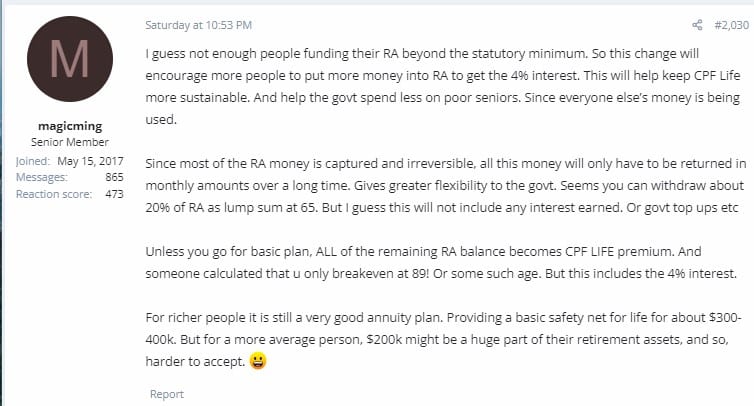

A netizen speculates that the policy change is intended to encourage more individuals to contribute additional funds to their RA beyond the statutory minimum, aiming to avail the 4% interest rate.

This, in turn, is seen as a measure to enhance the sustainability of CPF Life and reduce government spending on supporting financially challenged seniors.

PRs unaffected by recent CPF policy adjustments

Certain comments have pointed out that Permanent Residents (PRs) are less affected by the recent changes, given their ability to withdraw CPF at any time upon closing their account, unlike Singapore citizens.

This has led to the belief that the recent policy alterations might provide fewer incentives for PRs to convert to Singapore citizenship.

The forum member went on to claim that a colleague from China retired in China with S$1 million in CPF.

The self-proclaimed property agent mentioned observing numerous cases with substantial CPF amounts.