Retiree in Singapore deceived into investing S$180k with savings and loan

In the past 2 years, at least 5 vulnerable seniors in Singapore, including a 63-year-old retiree, were misled into investing a significant sum of money. Online users urged banks to compensate victims and tighten regulations to prevent exploitation.

SINGAPORE: At least five “vulnerable” seniors in the community fell victim to mis-selling tactics, ultimately leading to financial loss in the last two years.

Among these individuals, one retiree, aged 63, lacking proficiency in English and possessing only primary school education, was deceived into investing a substantial portion of his savings, totaling S$180,000, through a savings and loan scheme, as reported by The Straits Times (ST).

Initially he visited a bank with the intention of renewing his S$100,000 fixed deposit.

However, he was deceived into purchasing a more expensive insurance product, which entailed acquiring an S$80,000 loan despite lacking the means for repayment.

The bank representative allegedly provided false information, assuring him that the product would yield stable retirement income and dismissing repayment concerns by asserting that investment returns would cover them.

Assured of stable retirement income and led to believe that investment returns would offset any loan repayments, the retiree later discovered he had been misled.

After a year of not receiving any income and facing significant loan interest payments, he realized he had purchased an unsuitable product.

His loan repayments increased substantially, and the promised income did not materialize.

He sought assistance from the Financial Industry Disputes Resolution Centre (Fidrec), which ruled in his favor and directed the bank to compensate him for the mis-selling.

Such cases which involved retirees with limited education and poor English skills illustrate how easily vulnerable seniors can be targeted by unscrupulous sales staff.

Bank ordered to refund retiree in mis-selling dispute

Previously, the bank, which is not named, maintained that there was no mis-selling, citing that the retiree had signed all the documents, indicating awareness of taking a loan to fund the purchased product.

However, the retiree countered, stating that the forms inaccurately represented his education level, income, and experience in investment-linked policies.

During the adjudication process at Fidrec, the bank's manager failed to attend, and the bank's provided statement lacked detail and context. For instance, it didn't clarify whether the retiree received explanations regarding the product or the loan terms.

The adjudicator identified concerning aspects of the sales process, highlighting the lack of disclosure regarding the risks associated with borrowing money to fund the product purchase.

The adjudicator then ruled in favor of the customer, instructing the bank to refund the lost amount and the paid loan interest.

This troubling incident isn't isolated, with a total of 76 similar cases reported over the past two years, ST reported.

Despite efforts by the Monetary Authority of Singapore (MAS) to shield vulnerable consumers, instances of mis-selling persist, prompting concerns regarding the efficacy of existing regulations, particularly those requiring additional verification steps for individuals over 62 years old who lack proficiency in spoken or written English, to ensure they fully comprehend the risks and benefits involved.

Online users' responses

Looking at the comments on ST's Facebook post, a considerable portion of users express the belief that banks should indeed provide compensation to victims in such cases.

"The banks must take responsibility as long as the transaction took place in their premises," one user wrote.

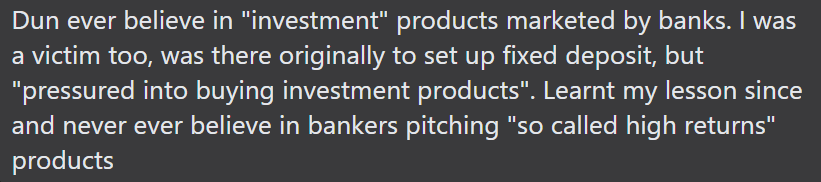

A user who reported experiencing a similar situation advised against placing trust in the "investment" products promoted by banks.

"I was also a victim," the user stated, elaborating that they were "pressured into buying investment products" despite initially intending to solely establish a fixed deposit at the bank.

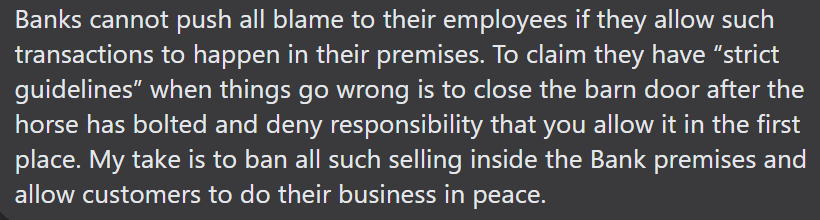

Others, however, argue that banks cannot absolve themselves of all responsibility by solely blaming their employees when such transactions occur on their premises.

They advocate for prohibiting such sales within bank premises to ensure customers can conduct their business without disruption.

Meanwhile, another asserted that banks should never be permitted to sell insurance or investments.

They argued that since banks have access to customers' account balances, such sales should not be permitted in the first place.

Some online commenters in the comment section also noted that incidents like this could occur to individuals regardless of their age or level of education.

"Even educated (people) can get scammed by banks," remarked one user, who disclosed their own experience as a victim.

"The bank staff claimed I mis-understood her," the user added, and was told that: "Sir... you already signed on the dotted line."

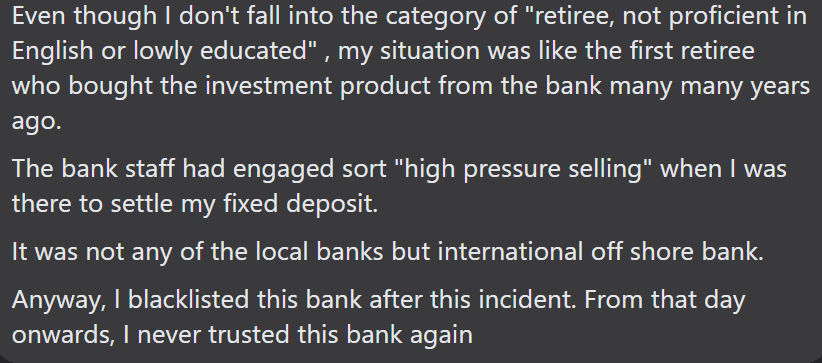

Another user also shared their experience, alleging that a bank employee resorted to what they described as "high-pressure selling" tactics while they were simply there to arrange a fixed deposit.