WP Jamus Lim responds to 'mean tweets' on loss-sharing for digital scam losses

In an Instagram video, WP MP Jamus Lim responds to 'mean tweets' and netizen queries about his loss-sharing proposal, emphasizing the sound rationale behind limiting losses faced by victims in the digital landscape.

Associate Professor Jamus Lim, Workers’ Party Member of Parliament for Sengkang GRC, has earlier advocated for a comprehensive approach to address the growing crisis of confidence in Singapore’s digital systems.

During the parliamentary debate on digital safety on 10 January, Assoc Prof Lim scrutinized the shortcomings of the Shared Responsibility Framework (SRF) in effectively addressing losses suffered by victims.

He proposed a more equitable sharing model, suggesting that telecommunications companies and banks assume a share of the losses incurred by consumers.

He introduced the idea of an insurance (and reinsurance) market as a potential solution, to limit liability and cap customers’ exposure to a predefined amount, such as S$100 or S$500.

Despite these proposals, there has been some resistance to Jamus Lim's loss-sharing idea.

In response to 'mean tweets' and questions from netizens, he provided additional insights via a video posted on his Instagram and Facebook account, further explaining why he believes that limiting the losses faced by victims remains a sound and justifiable idea.

Debating the user's role in digital scam losses

For example, a comment suggests, If users play an active role, even unwittingly, they should bear a fair share of the losses.

However, the argument against putting a blanket loss cap of S$100 to S$500 asserts that it might increase users' risk appetite.

In response, while agreeing that users should bear part of the losses, Assoc Prof Lim proposed a "thought experiment": What if the cap was S$1,000 to S$5,000?

He believed that people might agree with the principle of limiting losses, highlighting how moral hazards don't capture all the concerns.

"So, what it then comes down to is the extent to which this co-sharing of loss should be."

Assoc Prof Lim referred to the US, where fraud insurance has been in place for decades with a US$50 limit, noting that a S$100 or S$500 cap in Singapore is already higher.

Another netizen called Lim's idea "populist" and suggested that private corporations like banks and telcos would pass the cost down to consumers if forced to bear the last cost.

Assoc Prof Lim acknowledged the truth in this statement. He concurred that if financial institutions bear some of the losses, there will inevitably be a passing down of costs.

However, he underscored the importance of an insurance program as a counterbalance, drawing on global examples where limited losses have fostered the development of robust financial ecosystems.

Lim emphasized the potential benefits of such a system, aiming for fairness and protection for consumers in dealing with scams.

"This is ultimately what I hope to be able to see a robust system in Singapore for dealing with scams, rather than one with a little guy, in this case, the consumer ends up very essentially most of the cost. "

Global approaches to protecting consumers from scams

Meanwhile, another comment criticised that loss-sharing could simply embolden scammers around the world to target Singaporeans even more, suggesting that foreign banks will leave Singapore and set up shop elsewhere because of such a policy.

Addressing the concerns, Assoc Prof Lim pointed out that similar schemes are proposed globally.

For instance, in the UK, the current proposal is not even to limit it to $100 or $500 but, as long as the consumer has taken reasonable steps to avoid losses, they will bear zero.

In the US, where credit card fraud insurance has limited losses to $50 for 30-40 years, there hasn't been an exodus of banks.

"So I think it's more of asking ourselves, why is it that other countries have thought that it is sufficiently important to protect the consumer, whereas we feel that: No, actually consumers should be the ones that they are all the losses, " added Jamus Lim.

Netizens sceptical on current framework on scam protection

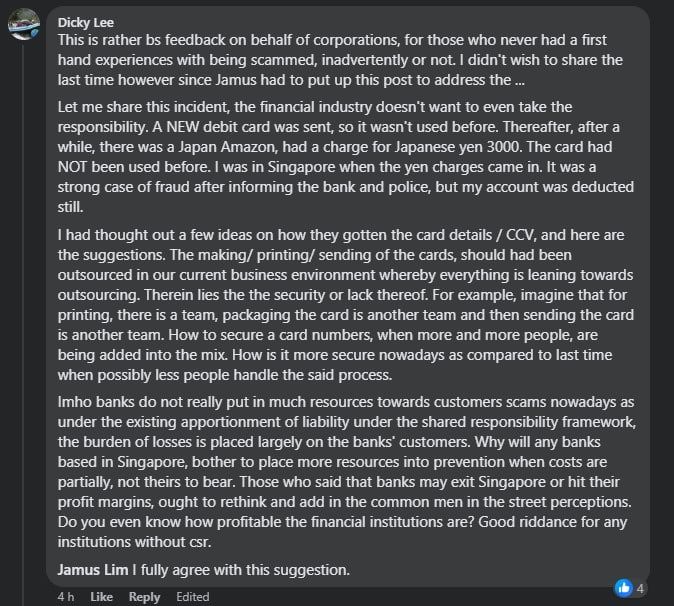

Observing comments on Assoc Prof Lim's social media account, netizens raise doubts about the effectiveness of the shared responsibility framework, noting that banks may not invest enough in preventing scams when the burden of losses is primarily on customers.

A netizen shared an incident where a new debit card, unused before, incurred fraudulent charges in Japanese yen.

Despite reporting the fraud to the bank and police while being in Singapore during the unauthorized transactions, the account was still deducted. The netizen expressed concerns about the security of card details and CCV, suggesting that outsourcing in the current business environment could compromise security.

In the netizen's opinion, banks allocate insufficient resources to address customer scams due to the shared responsibility framework, " Why will any banks based in Singapore, bother to place more resources into prevention when costs are partially, not theirs to bear. "

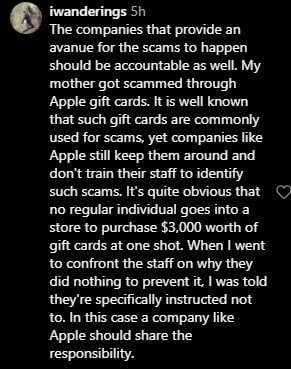

Another comment on Instagram highlighted the accountability of companies that provide avenues for scams.

The netizen shared a personal experience where her mother fell victim to a scam involving Apple gift cards, " It is well known that such gift cards are commonly used for scams, yet companies like Apple still keep them around and don't train their staff to identify such scams."

The netizen questioned the lack of preventive measures, especially when a substantial amount of gift cards is involved, and noted that confronting the staff revealed they were instructed not to intervene.

A netizen highlighted the internalization of a negative externality in the context of fraud protection by financial institutions in Singapore. He argued that the consumer bears the entire cost of fraud and scams, leading to a lack of investment in robust fraud protection measures.

The netizen shared a personal experience of finding unauthorized transactions on credit cards, despite taking precautions, and expressed frustration over the time and effort spent rectifying such issues.