"Cooling measures" or new policies to help the rich buy HDB resale flats?

Opinion: The increase in resale HDB flat grants to S$230,000, compared to just S$120,000 for BTO flats, raises questions about fairness. Wealthier buyers face fewer hurdles, while lower-income families must wait years for a BTO flat. The recent Loan-to-Value (LTV) ratio cut from 80% to 75% may also disproportionately impact the less affluent.

CORRECTION NOTICE:

This post contains a false statement of fact.

For the correct facts, visit: https://www.gov.sg/article/factually260824-b

by Leong Sze Hian

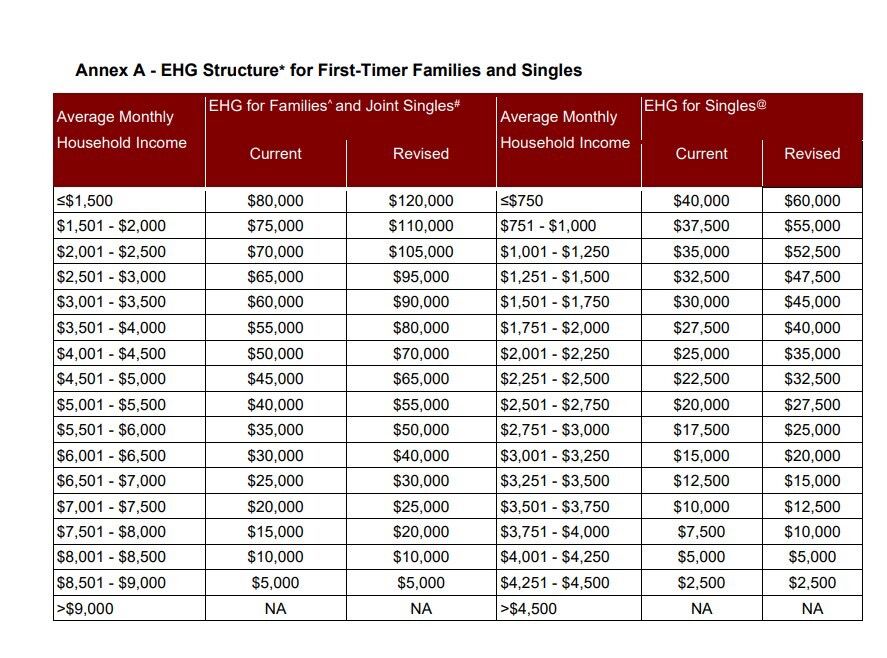

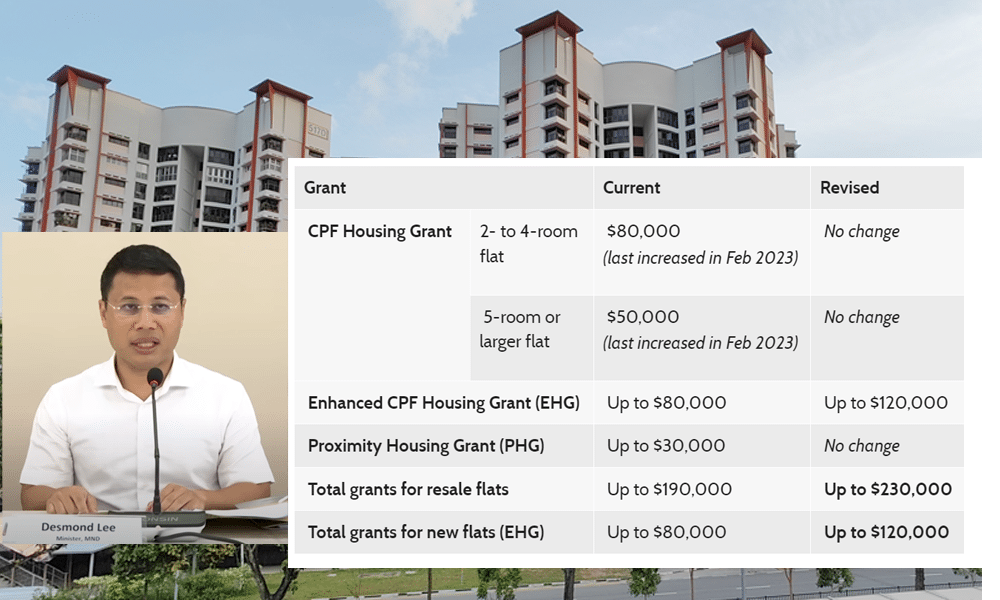

The maximum housing grants for Build-To-Order (BTO) flats have just been increased to S$120,000, with eligibility based on income means testing—households with an income not exceeding S$1,500 can receive the maximum grant of S$120,000.

In stark contrast, the maximum grant for resale flats has been increased to S$230,000, and there is no income means testing. The only requirement is that the household income ceiling must not exceed S$14,000 (S$9,000 in order to get the maximum grant of S$230,000).

For instance, households with an average monthly income of S$8,501 to S$9,000 receive only a S$5,000 grant for BTO flats, while those with a household income just below S$14,000 can receive up to S$230,000 in grants for resale flats (S$9,000 in order to get the maximum grant of S$230,000).

This raises an important question: Why are we providing more substantial financial assistance to, arguably, wealthier individuals to purchase more expensive resale flats, while offering less to those who may only be able to afford BTO flats?

For instance, households with an average monthly income of S$8,501 to S$9,000 receive only a S$5,000 grant for BTO flats, while those with a household income just below S$14,000 can receive up to S$230,000 in grants for resale flats.

Moreover, the recently announced decrease in the Loan-to-Value (LTV) ratio from 80% to 75% may have little impact on wealthier individuals, who can still comfortably finance their purchases.

In fact, in many cases, the 5% reduction in LTV for resale buyers may be outweighed by the S$40,000 increase in the grant.

For example, a reduction of S$50,000 in LTV for a loan up to S$800,000 may be less significant than the S$40,000 grant increase. This raises the question of whether this is truly a "cooling measure" or if it actually benefits wealthier buyers even more.

This further highlights the disparity, as those with greater financial means are less affected by such changes, making it easier for them to take advantage of the substantial grants for resale flats.

Furthermore, is it fair or equitable to have public housing policies that allow wealthier individuals to buy resale flats immediately (with up to S$230,000 in grants), while those with lower incomes must undergo income means testing to determine the grant amount, participate in a ballot, and potentially wait 4 to 5 years for a BTO flat?

It seems that for wealthier individuals, buying a resale flat may be a straightforward decision—qualify for up to S$230,000 in grants, hold the property for the Minimum Occupation Period (MOP) of 5 years, and potentially sell it for a profit. This profit would then be credited to their Central Provident Fund (CPF) accounts, along with the grant amount and accrued interest.

Are there any other public housing policies worldwide that, arguably, facilitate wealthier individuals in speculating and profiting more easily (such as upgrading to private property), while those with lower incomes may have to remain in Housing & Development Board (HDB) flats for most of their lives? These HDB flats typically decline in value after 40 years and become worthless at the end of the lease, meaning all the CPF savings and cash invested in the flat would be lost.

Perhaps we should explore and consider alternative and sustainable policy changes to mitigate the rising costs of both BTO and resale HDB flats.

For instance, we could gradually reduce the land cost component in the price of BTO flats or restrict Permanent Residents (PRs) from purchasing HDB resale flats.